In this post I'll do the same but for the DFM General Index.

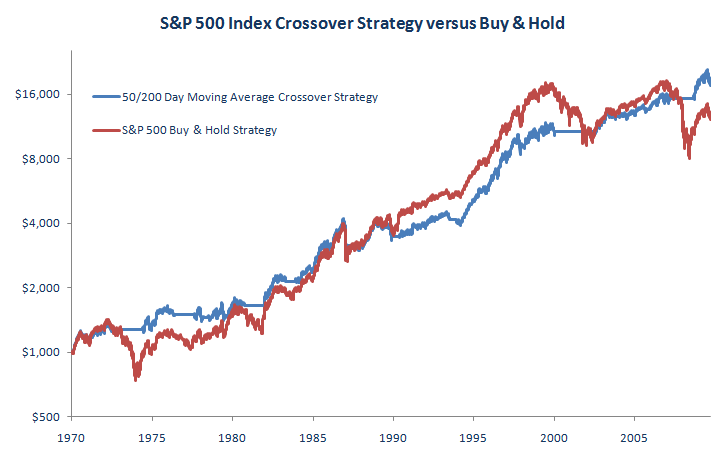

To recap, the main characteristics of the crossover strategy when applied to the S&P 500 were its ability to generate similar, long-term returns to buy and hold but achieving this with significantly reduced drawdowns and less time spent invested in the market.

OK, let's apply this strategy to the DFM General Index and see if the same conclusions apply. Firstly, below is a chart showing the 50-day and 200-day moving averages for the DFM:

Just by eyeballing the buy and sell signals on the chart above it appears that the crossover strategy did a good job of avoiding the worst market declines over the past five years. However, for a more accurate picture below are the P&L chart and performance statistics (Note: starting capital = $1,000, profits are reinvested, results do not include fees, slippage or dividends):

In interpreting these results above it is important to note a couple of things. Firstly, the 50/200 day moving average crossover strategy is a long-term trading system. For example, when applied to the S&P 500 Index the strategy only generated 20 trades over the last forty years. Now, the DFM General Index, indeed the entire DFM market, has only been in existence since the beginning of 2004. This doesn't give us a lot of data to work with when testing a long-term strategy and this should borne in mind when evaluating the results.

Secondly, the DFM General Index cannot be directly traded. At present, there is no instrument that exists which tracks the DFM index so the test results are very much hypothetical. That said, if the results are similar to the ones generated by the S&P 500 test they should provide us with a good indication of when to be in the market and especially when to get out of the the market. This will most likely be applicable to the underlying stocks in the DFM Index.

OK, what do the test results for the DFM General Index tell us? Over the test period the crossover strategy generated a annualised return of 22% compared with -3.70% for buy and hold. That's a big outperformance. However, most of the returns for the crossover strategy were achieved in 2004 (that's why the blue P&L line for the crossover strategy obscures the red P&L line for the buy and hold strategy). Since the the bull market ended in 2005 the strategy has not made any significant returns but it has done the next best thing by avoiding some really nasty falls in the market.

As can bee seen from the performance statistics, the worst drawdown for the crossover strategy was -45%. On it's own that's a pretty big drawdown to handle. However, when compared with the -83% drawdown the buy and hold strategy suffered it starts to look a lot better. The crossover strategy had a much lower average drawdown of-25% versus -45% for buy and hold.

Conclusion

All in all these results are similar in nature to those for the S&P 500 Index. The 50/200 day moving average crossover strategy managed to sidestep the worst of the market declines, declines which have been substantial for the DFM General Index over the last five years. This is has meant that the strategy has only been invested for just over 50% of time since 2004.

Unlike the S&P 500 Index results, the crossover strategy on the DFM General Index managed to significantly outperform buy and hold. However, this is probably because the test period for the DFM strategy was much shorter and was dominated by bear markets during which the crossover strategy was able to easily outperform buy and hold.

Next, I'll apply the 50/200 day moving average crossover strategy to other GCC indices and in later posts I'll test the crossover strategy but with different moving average lengths.

Enjoy.